Your Brain Is Lying to You About Risk How negativity bias is quietly killing your best ideas — and what Florida business owners should do about it

Picture this: You’re sitting at your desk on a Tuesday evening, and an idea surfaces. Maybe it’s a new service offering you’ve been turning over for months. Maybe it’s a completely different market you could reach with what you already do well. For a moment, it feels exciting — the kind of clarity that doesn’t come often. Then, almost immediately, the mental prosecution begins. The market probably isn’t ready. You don’t have the bandwidth. Someone has likely tried it already. What if your existing clients find out and question your focus? What if you invest real time and it goes nowhere? Within ten minutes, the idea is back in the drawer, and you’ve returned to whatever was on your screen before.

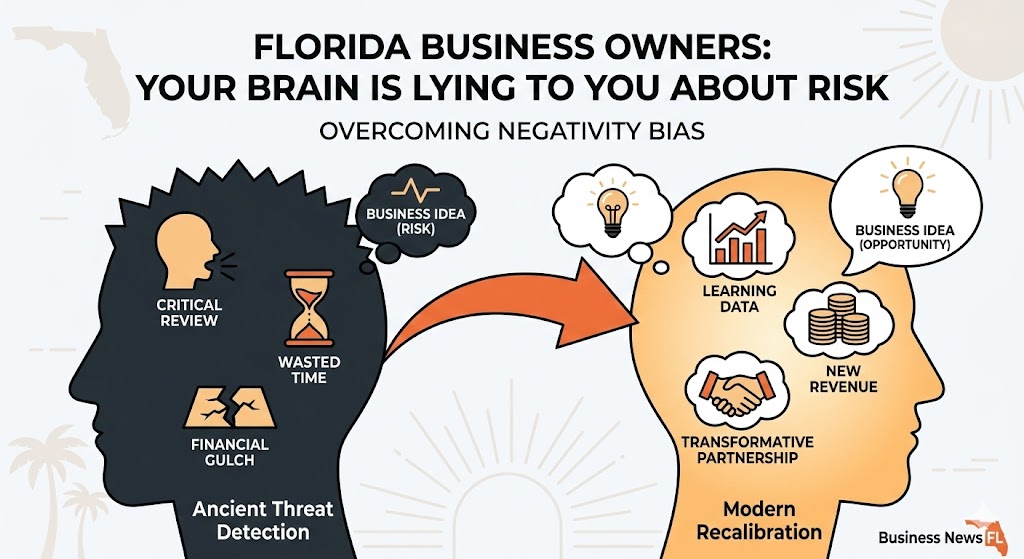

Here’s what’s worth understanding about that sequence of events: the voice that killed your idea wasn’t reason. It wasn’t experience. It wasn’t even genuine caution. It was a neurological inheritance from ancestors who lived in a world where the consequences of a bad decision could end your life before sundown. That mechanism kept the human species alive for hundreds of thousands of years. Today, in the context of a business idea that costs almost nothing to test, it is working directly against you.

For Florida’s business owners — operating in one of the most rapidly evolving, opportunity-rich economies in the country — this ancient wiring carries a modern price tag that most people never stop to calculate.

Wired for Danger: Where Negativity Bias Comes From

Negativity bias is among the most thoroughly documented phenomena in psychological research. The core finding is consistent across decades of study: the human brain assigns significantly more weight to negative experiences, outcomes, and information than to positive ones of equivalent magnitude. Negative events are processed more deeply, remembered more vividly, and felt with roughly twice the emotional intensity of comparably scaled positive events.

This is not a personality trait or a sign of pessimism. It is structural — wired into the architecture of how human brains evolved to process the world. And the reason it exists is straightforward: for the vast majority of human history, the cost of missing a threat was catastrophically higher than the cost of overreacting to one.

Consider the environment our ancestors navigated daily. A sound in the underbrush might be nothing. Or it might be a predator. If you assumed it was nothing and you were wrong, the outcome was fatal and final. If you assumed it was a threat and you were wrong, the outcome was a wasted burst of adrenaline and a short, unnecessary sprint. In a world structured by that asymmetry, the brains that survived were the ones that erred dramatically on the side of threat detection — the ones that treated ambiguous signals as danger, that scanned for what could go wrong before cataloguing what could go right, that weighted negative possibilities far above their statistical likelihood because the downside of being wrong was simply too severe.

Those are the brains that got passed down. Those are the brains we’re all running on today.

The legacy shows up everywhere once you start looking for it. It’s why a single critical comment in a performance review can overshadow fifteen positive ones. It’s why potential losses motivate behavior more powerfully than equivalent potential gains — a well-established principle in behavioral economics known as loss aversion. It’s why negative news dominates media consumption, and why a business owner can walk away from a strong quarter and spend the week mentally replaying the one client complaint rather than the ten expressions of satisfaction. The brain is doing exactly what it was designed to do. The problem is that the design spec is roughly 200,000 years out of date.

The Modern Mismatch: Threat Detection Without the Threats

The trouble isn’t that negativity bias exists. The trouble is that the human brain has no automatic mechanism for recalibrating it to the actual stakes of the situation at hand. The same neurological hardware that once protected our ancestors from genuine mortal danger now activates with nearly identical intensity when you consider emailing a prospect, testing a new pricing model, or sharing a half-formed idea with a trusted colleague.

When you sit down to honestly evaluate a new business idea — to weigh the genuine pros against the genuine cons — your negativity bias doesn’t function as a neutral risk filter. It functions as a prosecutor with a predetermined verdict. It makes bad outcomes feel vivid, textured, and near. It makes good outcomes feel abstract and distant. It disproportionately inflates the apparent probability of low-likelihood negative scenarios and compresses your intuitive sense of how likely success actually is.

Think about how this plays out in practice. An entrepreneur considers launching a complementary service line. The upside is concrete — additional revenue streams, a deeper client relationship, insight into an adjacent market, a competitive differentiator. But the negativity bias immediately populates the risk column with scenarios that feel urgent and plausible: What if execution is messier than expected and existing clients notice a dip in attention? What if the new offer gets mixed reception and damages the brand? What if a larger competitor sees the opening and does it faster and better? These concerns, even if they carry a realistic probability of perhaps 5 to 10 percent, receive something closer to 70 or 80 percent of the mental energy in the evaluation. The pro and con list looks balanced on paper. In practice, the cons have been written in a much larger font.

The analysis feels like careful thinking. It is actually pattern-matched threat response dressed up in the language of strategy.

Not All Downside Is Equal: The Immaterial Risk Problem

Here is where the gap between our evolved wiring and our actual circumstances becomes most consequential: in a remarkable number of idea-stage business decisions, the real downside of moving forward is genuinely, objectively immaterial.

Strip away the emotional weight for a moment and ask concretely: what does it actually cost to test a new service concept with a small subset of existing clients? What is the true exposure of sending a thoughtful outreach message to a potential strategic partner? What does it cost to build a simple one-page offer, share it with five people whose judgment you trust, and see what comes back? In the vast majority of cases, we’re talking about a few hours of focused time, perhaps a modest amount of money for a basic experiment, and a small quantity of professional goodwill. If the test doesn’t pan out, you gather information and redirect. There is no bankruptcy filing. There is no permanent damage to your professional reputation. There is no material loss of any kind that you wouldn’t recover from in short order.

What there is, and what the brain consistently refuses to categorize correctly, is emotional risk. The fear of looking foolish to people whose opinions you respect. The discomfort of being uncertain about an outcome you’ve committed to pursuing. The particular sting that comes from trying something that doesn’t work, especially if you told anyone about it beforehand. These feelings are real. They arrive with genuine force. For many people, they are significant enough to stop the attempt entirely.

But here is the distinction that changes everything: emotional risk and material risk are not the same thing. Negativity bias collapses them into a single category and processes both with the same alarm intensity. The entrepreneur who is afraid her new offer might get a lukewarm reception is not facing the same threat as the hunter who misread the sound in the underbrush. The stakes are incomparably lower. The consequences of being wrong are temporary, recoverable, and ultimately instructive. The brain, without deliberate intervention, will not make this distinction on your behalf. It is your job to make it consciously.

Before dismissing any idea on the grounds that it feels risky, ask one question with as much specificity as you can manage: if this fails, is the outcome material? If you can honestly answer no, you’ve identified something important — you are not weighing risk. You are managing an emotion. And emotions, unlike financial ruin, are something you can work through.

The Idea Economy: Why Asymmetric Upside Changes the Math

Florida’s economy is in the middle of a genuine transformation. What was once understood primarily as a state built on tourism, real estate, and seasonal industries has become something considerably more complex and dynamic. Tampa Bay has developed a legitimate startup and innovation ecosystem that is attracting outside attention and serious capital. Miami has emerged as a credible challenger to established coastal tech hubs, drawing venture funding, remote talent, and founders who want the energy of a major city without the cost structure of San Francisco or New York. Orlando has diversified well beyond its theme park identity into simulation technology, aerospace, and digital media. Across the state, the underlying engine is increasingly driven by ideas, services, and intellectual capital rather than physical assets and fixed infrastructure.

This shift matters enormously for how business owners should think about risk, because the economics of idea-based risk-taking are fundamentally different from the economics of capital-intensive risk-taking.

When a restaurant fails, the owner absorbs the full weight of a very real and very specific financial loss — the buildout, the equipment, the lease obligations, the working capital that’s now gone. When a manufacturing operation struggles, the downside is concrete and often severe. These are businesses where the risk is symmetric, where the capital committed creates a genuine floor of potential loss, and where the stakes of being wrong are materially high. Negativity bias, in those contexts, is doing something reasonably useful. It is flagging real consequences that deserve serious weight.

But when a Florida business owner tests a new consulting offer, explores a technology-enabled service model, pitches a creative market approach to a potential partner, or invests a few weeks developing and testing a digital product — the risk structure looks completely different. The downside is bounded and recoverable. The upside, however, can be genuinely transformative: a new revenue vertical that runs with minimal ongoing cost, a client relationship that expands to touch multiple parts of your business, a product that scales without requiring proportional increases in your time or overhead. The asymmetry runs strongly in favor of attempting.

In environments with that structure, the rational strategy isn’t caution. The rational strategy is volume. Pursue as many serious, well-considered idea-stage experiments as you can intelligently manage. If ten experiments yield two meaningful wins, the math is strongly in your favor. If twenty experiments yield four wins and one breakthrough, the math is extraordinary. The idea that you should sit on a potentially high-value concept until the conditions are ideal, or until the risk feels adequately reduced, is a strategy that sounds prudent but produces compounding underperformance. Every untested idea is an option you let expire.

A Framework for Taking More Idea Risk — Without Being Reckless

None of this is an argument for abandoning judgment or charging recklessly at every notion that occurs to you over coffee. It is an argument for developing a more calibrated and honest assessment process — one that accounts for the systematic bias your brain brings to the table and deliberately corrects for it.

Start by separating material from immaterial risk. When an idea surfaces, resist the urge to immediately begin evaluating it. First, spend two minutes honestly answering one question: what does the realistic worst case actually look like, in specific and concrete terms? Not the catastrophic worst case that your negativity bias will volunteer eagerly, but the likely worst case. If the answer centers on emotional discomfort — embarrassment, awkwardness, the mild frustration of a failed attempt — name it clearly and explicitly as an emotional risk, not a financial one. That single act of honest categorization will change how you proceed.

Audit your probability estimates before committing to them. Negativity bias doesn’t just amplify the intensity of bad outcomes — it inflates their perceived likelihood. If a scenario you’re worrying about has a realistic probability of 5 percent, but you’re allocating 40 percent of your decision-making energy to it, your assessment is distorted. Force yourself to assign rough probabilities to the scenarios in your pro and con analysis and examine whether the weight you’re giving them actually corresponds to their likelihood.

Build a live idea pipeline and keep it moving. One of the most effective structural corrections to negativity bias is changing the way you relate to ideas at the conceptual stage. Instead of treating each idea as a high-stakes individual bet that needs to clear a significant internal threshold before you act, treat your idea pipeline as a portfolio of small, fast, low-cost experiments that you run continuously. The goal is not to find the one perfect idea and execute it flawlessly. The goal is to run enough experiments that the wins, which will come, have a chance to surface.

Reframe explicitly what a failed experiment means. In an idea-driven economy, a well-designed experiment that doesn’t produce the hoped-for result is not a failure — it is paid tuition on the path to a better understanding of your market. The business owners who build the most durable advantages are not the ones who avoid failure most skillfully. They are the ones who cycle through small, inexpensive failures most efficiently, extract the signal from each one, and apply it forward. Florida’s most successful founders and entrepreneurs will largely confirm this from their own experience.

The Opportunity Cost No One Calculates

There is a cost to excessive caution that never appears on a profit and loss statement, never shows up in a business review, and rarely gets discussed in the same breath as financial risk. It is the compound cost of the ideas you didn’t pursue, the markets you didn’t enter, the offers you never made, the partnerships you never initiated, the experiments you shelved before they had a chance to teach you something.

This invisible ledger accumulates quietly. A year passes and your business is doing fine — revenue is stable, clients are reasonably happy, operations are under control. But it is also, in some essential way, exactly the same business it was a year ago. The ceiling hasn’t moved. The options haven’t expanded. And somewhere in a mental drawer is a collection of ideas that never got a fair trial because your brain presented the emotional risk of attempting them as though it were something far more dangerous than it actually was.

Florida’s business climate right now is genuinely conducive to idea-driven growth. Capital is flowing. Talent is relocating. New industries are establishing roots. The entrepreneurs who position themselves to take advantage of this moment are not going to be the ones who waited until the risk felt manageable. They are going to be the ones who understood clearly what was and wasn’t actually at stake — who learned to tell the difference between a real threat and an evolutionary alarm that no longer matches the environment it’s sounding in.

More Florida Business News:

• Insider Secrets: 5 Proven Strategies to Excel in Business School and Beyond

• Boca Raton Catering Services with Graze Craze

• Publishers Battle Florida’s Book Ban

• Florida News and PR Articles Links with Florida Website Marketing

• Boca Raton Women’s Boutique Wish & Shoes

Your negativity bias is not going away. It is too deeply embedded, too fundamental to how the human brain processes the world, to be switched off by an act of will. But it can be worked with consciously. It can be named, examined, and deliberately corrected for. And when you do that work — when you ask honestly whether the risk is material or emotional, when you audit your probability estimates rather than simply believing them, when you build the habit of small and relentless experimentation — you will find that the ideas you’ve been protecting yourself from were never as dangerous as they felt.

Most of the time, the idea sitting in your notebook costs almost nothing to test. The risk isn’t financial. It’s emotional. And that is a risk worth taking.